|

Sector Model

|

XLB

|

3.97%

|

|

|

Large Portfolio

|

Date

|

Return

|

Days

|

|

BBRY

|

7/16/2012

|

99.72%

|

313

|

|

CAJ

|

9/25/2012

|

5.26%

|

242

|

|

BOKF

|

2/4/2013

|

16.60%

|

110

|

|

SWM

|

2/12/2013

|

30.76%

|

102

|

|

MWW

|

4/11/2013

|

16.52%

|

44

|

|

ABX

|

4/11/2013

|

-21.67%

|

44

|

|

TPX

|

4/22/2013

|

-6.37%

|

33

|

|

TTM

|

5/6/2013

|

-3.87%

|

19

|

|

DLB

|

5/13/2013

|

0.64%

|

12

|

|

GMCR

|

5/24/2013

|

-1.41%

|

1

|

|

S&P

|

Annualized

|

10.82%

|

|

|

Sector Model

|

Annualized

|

25.83%

|

|

|

Large Portfolio

|

Annualized

|

32.05%

|

|

|

YTD

|

|

||

|

S&P

|

15.67%

|

|

|

|

Sector Model

|

24.23%

|

|

|

|

Large Portfolio

|

18.43%

|

|

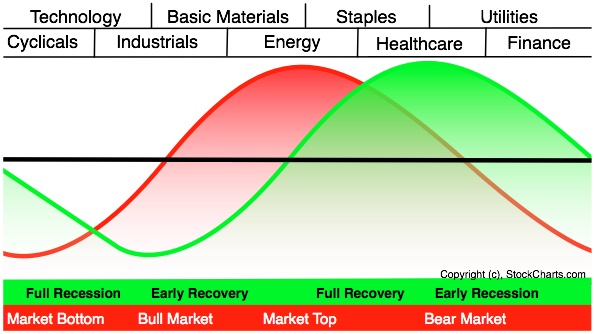

No rotation.

As you can see, the year to date performance of the sector

model is again outstripping the full portfolio.

Meanwhile the Mousetrap continues to evolve, and the fundamentals are

increasingly moving toward larger companies.

That makes sense, in light of the outperformance of the

sector model, since the sector ETFs are cap weighted indexes.

It also makes sense as a trend continues to mature and as

retail investors pile into stocks.

Of further note is the fact that the fundamental filters are

beginning to make more sense from a classical value perspective. These are right at the top of the selections:

|

Cash Flow Growth 5-Year

|

High

|

|

Sales Growth 5-Year

|

High

|

|

EPS Growth 5-Year

|

High

|

|

Est EPS 1st Qtr Out

|

High

|

|

Est EPS 2nd Qtr Out

|

High

|

|

Total Return 1-Year

|

Low

|

That translates to three things:

1) Earnings have usually been good

in the past, and are

2) estimated to be good in the future, but

3) the price is depressed right now.

That’s simpler than what the model was spitting out before.

Heck, even Buffet could do that.

As for the market, I can’t say what it’s GOING to do. I can only comment on what it seems to THINK

it’s going to do. It THINKS it’s going

to go back to its long term median regression.

That would take the current trend above 2000 in mid-2015.

Keep in mind that the market thought it would ride the long

term regression back in 2007 too.

A regression is great for estimating what the market will do

a few business cycles out, but can’t tell you anything about the next few

months. It’s like that Shiller Yield I

graphed a few weeks ago: fantastic for estimating ten year returns, and

worthless in any shorter time frame.

The ONLY meaningful use of the Shiller Yield is to compare

regional indexes for long term opportunities.

But don’t use long term estimates to predict the short

term.

And for goodness sake, don’t use the news!

99% of the market news articles have no idea what they are

saying in terms of tradable calls. I

know this because they usually tell me what I’m thinking myself, and my brain

can’t time its way out of a paper bag.

News articles have only one true goal – to sell news

articles.

It’s like politicians – their only goal is to get

re-elected.

Or judges – their only goal is to keep from being

overturned.

So, news articles will write what you want to read; politicians

will do what their donators demand; and judges will adjust justice in favor of whoever

has more money to pay for appeals.

They don’t even pretend to be interested in truth, justice,

or the American way.

What they ARE interested in, is money: news sales, political

contributions, the richest litigant.

If you want to predict the future, you only need to do one

thing: follow the money.

Investing works the same way: stocks make money when businesses

make money.

End of story.

Tim

{kind=link}