Small Portfolio

|

XLF & IAU

|

8.07%

|

|

|

|

|

|

Position

|

Date

|

Return

|

Days

|

GCI

|

7/14/2011

|

13.48%

|

360

|

CSGS

|

10/3/2011

|

40.43%

|

279

|

NLY

|

10/25/2011

|

11.23%

|

257

|

KBR

|

10/27/2011

|

-14.38%

|

255

|

VG

|

10/27/2011

|

-37.99%

|

255

|

BT

|

1/4/2012

|

7.34%

|

186

|

SAI

|

5/30/2012

|

4.96%

|

39

|

XEC

|

6/5/2012

|

6.91%

|

33

|

DECK

|

6/15/2012

|

-6.15%

|

23

|

CVX

|

7/5/2012

|

-2.14%

|

3

|

|

|

|

|

S&P

|

Annualized

|

0.64%

|

|

Small Portfolio

|

Annualized

|

7.29%

|

|

Large Portfolio

|

Annualized

|

8.38%

|

|

The small portfolio is having one of those weeks that waffles

back and forth between the leading sectors (right now XLV and XLF, healthcare

and financials).

The S&P is having one of those years that stumbles in

May and might recover again for the end of the year.

And the globe is having one of those decades that goes

nowhere.

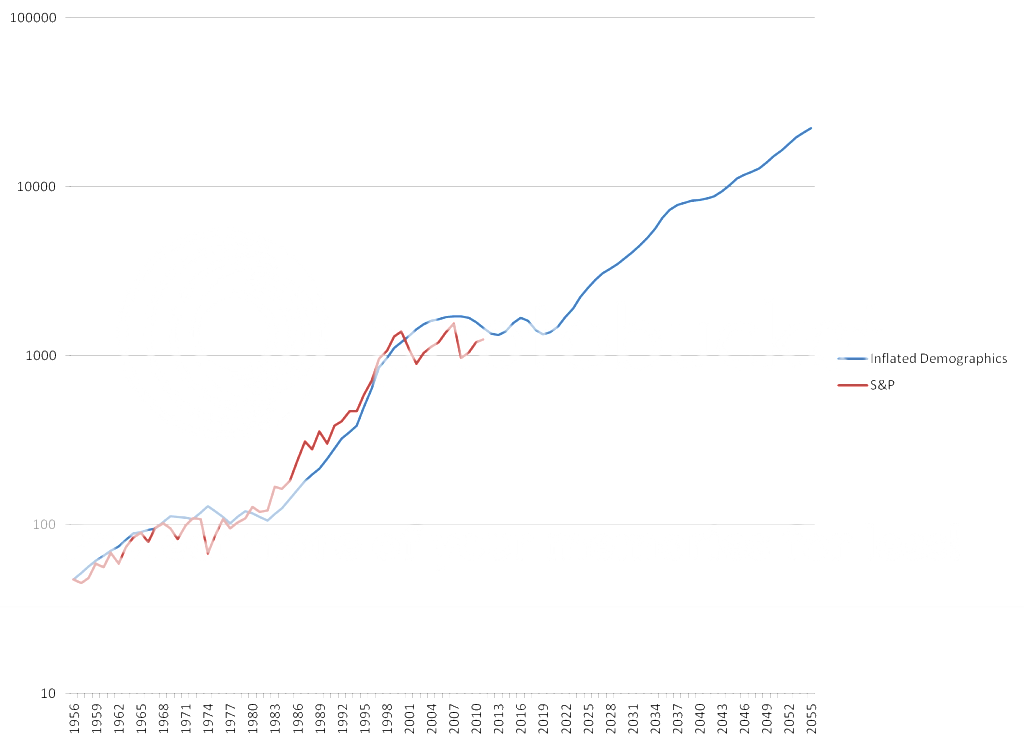

Here’s the long view of where the S&P will likely go:

Stocks represent businesses, and businesses are created by

people. If you factor inflation into the

birthrate 46 years ago you’ll get a graph like the one above.

I haven’t filled in the number for this year yet, but the

average S&P price for the year will likely not exceed the demographic limit

of 1346.55.

We probably won’t break out until 2017 or later.

To get an idea of how this works, imagine you owned a

manufacturing plant that had three sets of machines. One set is being built, the second set is

making your product, and the third set is broken from too much use. You only make money off of the machines that

are working. You lose money off of the

ones being built, rebuilt, or hauled off.

Now think of those machines as people. That’s where we are now. People 0-22 and people 65-120 don’t usually

have as many jobs as people 20-65. The birthrate

+ 46 years is just a quick way to get the average of those 22-65 year olds.

Welcome to a secular bear market: that dip that happens when

people didn’t have as many babies 46 years ago as they should have. The Beatles weren’t romantic enough to get

the job done.

The good news is that bonds are safe havens, right? Right?

Well, no. Interest rates are

about as low as they can go, and at some point they’ll have to rise, and bonds

will get slammed.

But the “supercycle” in gold will make us all rich if we

invest there, right? Right? Well, no.

Interest rates are as low as they are because the Fed is desperately

fighting deflation, and even a winning position in gold will basically leave

you with the same “value” you had to begin with, while you’ll get taxed off of

the inflation. If gold is your only

hold, you’ll still lose.

It’s either Carter or Hoover, and there’s no certain way to

tell which way it will go.

It’s safe to bet on Carter for now, though. Bernanke wants to keep his job, and all the

Republican nominees promised to fire him if they got elected. So, all Bernanke has to do to keep his job is

to keep pumping money into the system to keep things from collapsing before the

election.

That’s what I’d do if I were Bernanke. In this economy, you try to keep your job…

This is a bear market that will wipe you out if you try to

short it. Even the cyclical bear we are

in (and we ARE in a cyclical bear market, albeit a sideways one) refuses to go

down in nominal value because every central bank on the planet is printing

monopoly money faster than stocks can fall.

My guess is that this will continue for another year or two

before something starts to gain traction.

Value stocks had a crappy year last year. They’ll probably do better this year. Won’t make you rich, but they won’t send you

to the poor house either.

And gold will end the decade higher than now. But in the mean time where it goes is

anyone’s guess.

The key is to not get cocky with leverage. Bear markets cannot be predicted because of

the massive political forces and central bank intervention at play. It’s not good enough to just be right. You have to be disciplined with position

sizes so that you won’t get wiped out BEFORE you are right.

Every time I’ve ever lost money was in a position that

turned out to be right, but I wasn’t able to ride out the volatility.

The only thing to fear is greed. Control your own position sizes, invest in

sound companies, and you’ll survive.

Yes, a few people make wild bets and get rich.

We don’t hear about the vast majority of those who made

similar bets and lost everything.

Tim